What are the Largest Sole Proprietorships in the world?

Believe it or not, the Largest Sole Proprietorship in the world simply wouldn’t exist.

Unfortunately, Sole Proprietors don’t receive any Limited Personal Liability Protections.

This single factor means anybody with a significantly sized Sole Proprietorship would surely upgrade their Business type to a Single-Member LLC or Corporate variation as soon as humanly possible.

Without any liability protections, any massively successful sole proprietor would be out of their mind to NOT convert their business to one which provides the peace of mind of Limited Personal Liability Protections, the savings of tax breaks, and the option to expand and add Owners and Investors.

➤ MORE: Why do some sole proprietorships fail while others succeed?

What is the number of Sole Proprietorships in the United States?

According to the U.S. Census Bureau’s most recent report, there were 611,049 Sole Proprietorships in the US in 2022, a decrease of 223,662 from 2021’s count of 834,711.

➤ MORE: Why do some sole proprietorships fail while others succeed?

Compare this to the total 8,298,562 Business establishments in the US in 2022, up from 8,148,606 in 2021.

Key Takeaways

Key Takeaways

- Sole Proprietorships make up 10.24% of businesses in the United States

- Sole proprietorships are simple and low-cost, but owners are personally liable for all business debts.

- Reporting business income and expenses on personal tax returns simplifies tax filing.

- Expanding may require special financing or partnerships.

- Consider LLCs or corporations if you are looking for legal protection.

Table of Contents

Table of Contents

- What are the Largest Sole...

- What is the number of Sole...

- What percentage of businesses are Sole...

- Sole Proprietorship Tax Return...

- The 5 Strengths and Advantages of a...

- How many owners does a Sole...

- What is a successful Sole Proprietorship

- Why are Sole Proprietorships the MOST...

- What is a Major Weakness of the Sole...

- What are 3 trade offs of running a Sole...

What percentage of businesses are Sole Proprietorships?

Based on the 2022 Census data showing 611,049 sole proprietorships out of 8,298,562 total businesses, 7.36% of businesses are Sole Proprietorships in the United States.

It’s clear from this fact alone that a significant portion of people enjoy being sole proprietors in the US.

It should come as no surprise since they are the easiest, cheapest, and fastest business for someone to start.

➤ TAKE INITIATIVE: Here are some examples use can use to start your own Sole Proprietorship

Sole Proprietorship Tax Return Statistics from 2015 to 2022

Sole Proprietorship Statistics (Nonfarm)

| Year | Profitable Businesses Only | All Businesses | ||

|---|---|---|---|---|

| Number of Tax Returns | Net Income | Number of Tax Returns | Net Income Less Deficit | |

| 2022 | 21,967,453 | $543,895,820,000 | 30,983,810 | $410,664,065,000 |

| 2021 | 21,101,950 | $516,804,183,000 | 29,309,596 | $411,308,783,000 |

| 2020 | 19,976,748 | $436,416,303,000 | 28,353,367 | $337,201,262,000 |

| 2019 | 20,068,698 | $443,311,370,000 | 27,817,189 | $355,177,264,000 |

| 2018 | 19,634,588 | $429,990,931,000 | 27,117,163 | $348,509,654,000 |

| 2017 | 19,434,121 | $415,788,805,000 | 26,426,406 | $346,241,776,000 |

| 2016 | 18,959,230 | $389,138,987,000 | 25,525,915 | $328,209,453,000 |

| 2015 | 18,784,750 | $392,114,132,000 | 25,226,245 | $331,832,538,000 |

The 5 Strengths and Advantages of a Sole Proprietorship

- There’s no paperwork or State registration hoops to jump through

- Simplest and fastest business entity to set up

- You have total control over every facet of the business

- Dissolving the business is effortless

- The easiest taxation model: The Pass-Though Process

How many owners does a Sole Proprietorship have?

A Sole Proprietorship is a business structure where a single individual owns and operates the business.

With only one owner, this business entity offers unparalleled simplicity and direct control, making decision-making and operations straightforward.

The bad news is this single ownership also means owners are personally liable for debts and can face challenges in raising capital, as all responsibilities and risks fall on the sole owner.

What is a successful Sole Proprietorship?

Several famous companies began their journeys as sole proprietorships before growing into the large corporations they are today.

Here are five business’s you’ll probably recognizenotable examples:

1. eBay:

Founded by Pierre Omidyar, eBay started as a small online auction website operated as a sole proprietorship in 1995.

It quickly grew into a major online marketplace.

2. Kinkos:

This well-known business began as a sole proprietorship under the leadership of founder Paul Orfelea.

Despite its expansion, Kinkos maintained the sole proprietorship structure through various partnerships until it was eventually sold.

3. Annie’s Homegrown:

Started by Ann Withey, Annie’s Homegrown began as a sole proprietorship focused on creating and selling organic food products.

The company’s growth eventually led to its incorporation.

4. Walmart:

Long before becoming a global retail giant, Walmart started as a series of independent retail stores in Arkansas, founded by Sam Walton as a sole proprietorship in the 1950s and 1960s.

5. J.C. Penney:

James Cash Penney began his career as an employee in a small retail chain and eventually bought out the shares from the existing partners.

Initially, J.C. Penney operated as a sole proprietorship before incorporating about 25 years later.

These examples highlight how sole proprietorships, though simple and small at the beginning, can grow into large and successful businesses.

Why are Sole Proprietorships the MOST popular business entity?

As the simplest business entity to both set up and operate, it is no wonder why so many people opt for Sole Proprietorships as opposed to going through the headache of registering a business with your state.

Other, more complicated businesses (LLCs and Corporations) require a lot of upkeep and annual registration fees.

Honestly, the best part of a Sole Proprietorship is getting out of having to file stacks of paperwork and deal with government bureaucracy.

➤ MORE: Have a deeper look at the Sole Proprietorship's greatest attributes.

What is a Major Weakness of the Sole Proprietorship?

The main pitfall of starting a Sole Proprietorship is the limitations on what you can and cannot do.

For instance, it can be extremely difficult to secure funding as an unregistered, unrecognized business.

To put it in modern tongue…

You don’t have any clout while operating as a Sole Proprietor.

It’s also important to consider the amount of liability you take on as a Sole Proprietor.

Any debts or liability falls directly on you. Like it out not, you are “solely” responsible for every aspect of your business.

Banks can’t give you a business loan or business credit cards because, legally speaking, you don’t have a business.

You are just making money under your name by providing goods and services. There is no entity and no liability protection.

➤ MORE: What else is wrong with being a Sole Proprietor?

What are 3 trade offs of running a Sole Proprietorship?

1. Protection

The single worst aspect of the Sole Proprietorship as a business entity is it’s complete lack of liability protection.

In a nutshell, this means sole proprietors have to stick with low- or no-risk businesses.

If something goes wrong and the business gets sued or owes money to creditors, the sole proprietor is liable to pay out of pocket for all legal and business fees.

Not only does this personally affect the owner of the business, it also has a massive impact on their ability to secure funding.

If a Sole Proprietor wants to take out a loan, they cannot go to the bank and take out a business loan, they have to take out a personal loan.

If the Sole Proprietor decides to try and find private investors, they simply won’t risk more capital than what the sole proprietor is worth.

Due to their lack of protection Sole Proprietors are heavily restricted to what they sell and how they go about getting their business up and running.

2. Tax Options

If you are looking for a variable taxation structure to fit your business needs, stay away from the Sole Proprietorship.

You would be better off setting up an LLC, S-Corp, C-Corp, or Corporation.

Sole Proprietorships have one standardized tax setup:

The Pass-Through Process

With this setup all of the business’s profits are automatically “passed” on to the owner’s personal account.

Any profits (or losses) coming from the Sole Proprietorship are declared on the 1040-SC Form.

This is attached to the federal tax return and you’re good to go.

With a Sole Proprietorship you are paying Self-Employment tax in addiction to the usual federal, state, and local income taxes based on where you live.

Self-Employment tax is the IRS’s fancy name for when they combine Social Security and Medicare taxes.

The main difference between this standardized process and those of LLCs, S-Corps, C-Corps, and Corporations is these more complex business entities provide you the ability to split and mix these taxes in different ways.

These state-registered entities allow for tax optimization but with the simplified Sole Proprietorship you are stuck with the default tax structure.

3. Management Options

In a Sole Proprietorship you lose the ability to structure the business how you want.

You don’t have a choice on whether you want to be actively or passively involved in the business like you could with an LLC or Corporation.

The more complex businesses give you the option to be more hands-on and involved in the day-to-day decision making in the company.

They provide you the ability to be totally hands-off and hire a management team to do all the nitty-gritty work for you. You would still be involved in all major company decisions either way.

Having a management team allows you to take a step back and focus on the big picture vision instead of losing sight and getting distracted with all the little things which inevitably come up.

This is not the case in a Sole Proprietorship.

In stead of getting the chance to be hands-off, you have to be all hands on deck.

Sole Proprietorships only exist if the owner, the sole proprietor, is actively managing and operating the business themselves.

Sole proprietors can hire employees if they want, but the owner have to be a part of all decisions, both short- and long-term.

➤ MORE: Why are LLCs so popular?

How long does a Sole Proprietorship last?

Sole Proprietorships last until one of three events occur…

1. The owner dies,

2. The sole proprietor stops providing whatever products or services they sell or,

3. The owner has the option of selling the components of the business like their tools, inventory, or equipment and is therefore unable to continue business operations.

Being that the Sole Proprietorship is the simplest business entity, it is completely reliant on the owner and their ability to keep their business up and running.

As soon as the owner dies or stops doing business, the Sole Proprietorship dissolves.

What are the largest sole proprietorships in the world?

The largest sole proprietorship in the world is difficult to determine because sole proprietorships are typically small, privately owned businesses, and they do not have to disclose their financial information to the public.

Additionally, the definition of “largest” can vary, whether it’s based on revenue, profits, or number of employees.

However, it is widely believed that Cargill, a global food corporation based in the United States, was once the largest privately-owned sole proprietorship before it incorporated in 1961.

Today, it is one of the largest privately held corporations in the world, but it is no longer a sole proprietorship.

In general, sole proprietorships are more common among small businesses.

It is rare to find very large businesses operating under this structure.

This rarity is due to the limitations and risks associated with sole proprietorship, including:

-

Unlimited personal liability.

-

Difficulties in raising capital.

➤ Explore: 17 of the most profitable of Sole Proprietorship businesses

Despite the challenges of operating as a sole proprietor, strategic tools like custom pens and branded merchandise can help boost brand awareness.

A well-designed custom pen acts as a mobile billboard, keeping a business top-of-mind while encouraging word-of-mouth marketing.

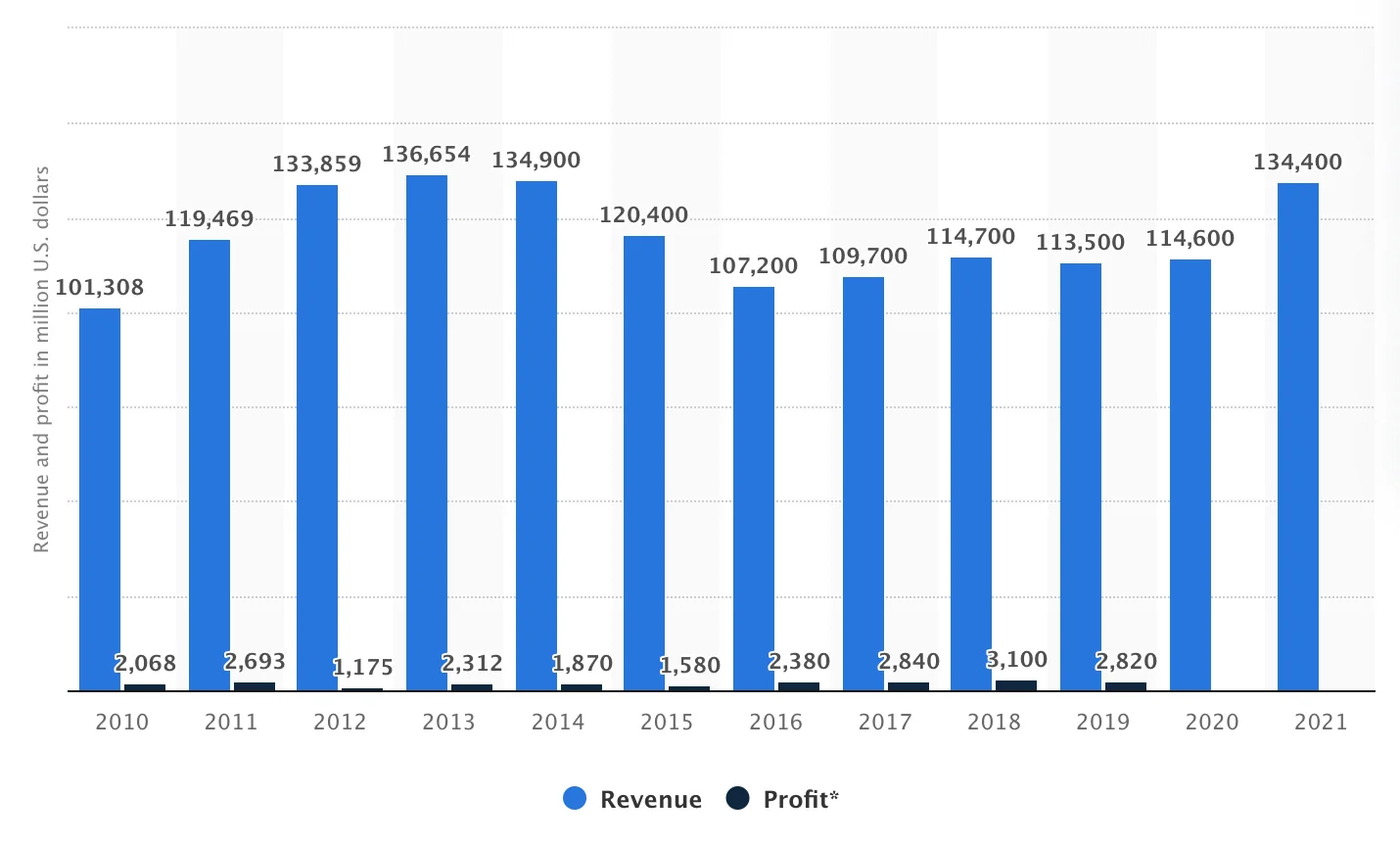

What is the richest privately owned company?

Although Sole Proprietorships are known to be better for side-hustles and small, low-risk operations some can get quite big before the owner decides to register it as an LLC or get the stamp of approval from the state and turn it into a Corporation.

With that being said…

Cargill is the biggest privately owned corporation in America coming in at an annual revenue of $165 Billion, according to their 2022 Annual Report.

This food production giant was started way back in 1865 and currently employees 155,000 workers worldwide.

Based on their wikipedia page, Cargill brought in a net profit of $4.93 Billion in 2021, after material costs and taxes.

Being a private company, Cargill restricts access to their financial reports.

Here is what they’ve released so far:

5 Facts About Sole Proprietorships?

1. Single Owner Business

Sole Proprietorships are limited to one owner who doubles as the main operator.

➤ DISCOVER: How to ensure your business is a successful endeavor!

2. Business Assets are Personal Assets

This type of business doesn’t separate between the business and it’s owner.

This goes for everything in the business including all profits and liability.

Whatever the sole proprietor makes from the business is immediately catalogued as personal gains.

If the business takes on any risk or liability in the form of debts, the responsibility falls completely on the owner to pay it back.

The unfortunate reality is if the owner is unable to pay back loans from their business and it’s profits, the owner then has to pay out of pocket.

This means the bank can come after the owner’s personal assets and property in order to repay what is owed.

3. Total Control

Since the owner is viewed as the business from a legal standpoint, they have full control over every aspect of the business. All decisions are made by the sole proprietor.

However, this is a bit of a double edged sword.

On the one hand the owner gets all the credit and praise when things are going well and business is booming.

On the flip side, the owner is at fault should the business take any losses or make mistakes.

➤ Take Initiative: 17 ideas you can use to start your very own Sole Proprietorship TODAY!

4. Informal Business Structure

As the simplest business entity, Sole Proprietorships are not registered with the state.

All it takes to start one is to make money providing a service or product under your legal name.

This gets you out of having to file paperwork with your local government and pay registration, filing fees, and annual maintenance costs.

All of which have to be done when operating an LLC or Corporation.

5. Pass-Through Taxation

The money sole proprietors make is “passed-through” to their personal account.

This streamlines the entire taxation process.

All the owner has to do is account for any profits or losses on their personal income tax return.

The only additional piece of paperwork one has to complete is the 1040-SC Form.

Just attach this to the federal tax return you are probably already familiar with and complete every year.

How long do small businesses last?

The lifetime of a small business depends on many factors.

Variables like the market, the state of the economy, and a business’s profit margins can all have a massive impact on the sustainability of a particular business.

A company could also loose their customer base to a competitor or just die out because a newer or better version becomes available.

Most small business last until one of two events occur:

1. The small business ceases operation and closes it’s doors

2. The small business grows and expands to the point where it is no longer called a small business.

Let’s say you have a family owned auto repair shop and in comes a franchise location for a large corporate auto repair service.

Unless your small business can beat their prices and perform repairs better than your corporate competitor, the odds are stacked against you. But…

Maybe you and your mechanics have developed some groundbreaking technique to clean oil or change brakes or install new spark plugs better than the mainstream approach.

Your customer base could grow to the point where you begin expanding your business and opening up new locations.

Now your small business isn’t so small anymore.

What are 5 disadvantages of a Sole Proprietorship?

1. Sole proprietors are fully responsible for all aspects of their business.

Total liability prevents owners from taking the risks necessary for some businesses to flourish.

2. As the simplest business entity, owners are limited to one taxation method: The Pass-Through Process.

There are no tax breaks available for Sole Proprietorships like there are for LLCs and Corporations.

3. Without having to register with the state, Sole Proprietorships are generally viewed as inferior businesses compared to LLCs and Corporations.

This makes finding investors and establishing yourself as a credible business much more difficult than if you had an LLC or Corporation.

4. You cannot set up a business bank account because Sole Proprietorships are technically viewed as unofficial business entities.

5. Although they are relatively easy to dissolve, selling a Sole Proprietorship is extremely difficult.

You cannot sell the Sole Proprietorship as an entity because, from a legal point-of-view, its not a business entity.

The only way to sell the business is to sell the individual components, materials, and anything else necessary to the manufacture of the products or the ability to provide the services you sell.

➤ DISCOVER: Why you should avoid Sole Proprietorships like the plague.

Do Sole Proprietorships have unlimited life?

No, Sole Proprietorship entities will end when one of the following events occur:

1. The owner, known as the sole proprietor, decides to sell the materials and equipment necessary for the business to operate.

2. The sole proprietor chooses to stop running the business.

In a Sole Proprietorship the owner is legally viewed as the business itself.

If the owner is no longer present or is unable to continue providing their services or selling their goods then the Sole Proprietorship simply dissolves.

Just as the Sole Proprietorship is nothing without a sole proprietor to manage and operate the business, so to the business isn’t a business if it’s not productive.

FAQs - Answers to Frequently Asked Questions About Sole Proprietorships

What is a sole proprietorship?

A sole proprietorship is a type of business structure where an individual operates as both the owner and operator of the business.

The owner is personally responsible for all assets, liabilities, and taxes associated with the business.

Learn More...

A sole proprietorship is a business structure with one individual as the owner and operator.

The owner is personally responsible for all business-related assets, liabilities, and taxes.

How common are sole proprietorships?

Sole proprietorships make up 86.3% of nonemployer firms and 13.0% of small employer firms in the United States.

Learn More...

According to the latest U.S. Small Business Administration (SBA) 2024 data, sole proprietorships make up 86.3% of nonemployer firms and 13.0% of small employer firms.

With 28,477,518 nonemployer firms in the U.S., this means approximately 24.6 million sole proprietorships operate without employees.

What are the benefits of choosing a sole proprietorship business structure?

Simplicity, complete control, and tax advantages.

Learn More...

Benefits of a sole proprietorship include simplicity, complete control, and tax advantages.

- Simplicity: Setting up a sole proprietorship is relatively easy, with minimal paperwork and low startup costs.

- Complete control: As the sole owner, you have full authority over business decisions.

- Tax advantages: Business income and expenses are reported on your personal tax return, and there are no separate business taxes.

What are the disadvantages of a sole proprietorship?

Personal liability, difficulty raising capital, and limited growth potential.

Learn More...

Disadvantages include personal liability, difficulty raising capital, and limited growth potential.

- Personal liability: As the owner, you are personally responsible for all debts and legal liabilities incurred by the business.

- Difficulty raising capital: Sole proprietorships may face challenges in securing loans or attracting investors.

- Limited growth potential: The business structure can limit opportunities for expansion and diversification.

What are the tax implications of a sole proprietorship?

Business income and expenses are reported on the owner's personal tax return using Schedule C.

The owner is subject to self-employment taxes calculated using Schedule SE.

Learn More...

In a sole proprietorship, business income and expenses are reported on the owner's personal tax return using Schedule C.

The owner is subject to self-employment taxes, which include Social Security and Medicare taxes, calculated using Schedule SE.

How are sole proprietorships different from other business structures?

Sole proprietorships have one owner responsible for all aspects, while other structures vary in ownership, liability, and tax treatment.

Learn More...

- Partnership: A partnership involves two or more people sharing ownership and management responsibilities, as well as profits and losses. In contrast, a sole proprietorship has only one owner who assumes all responsibilities.

- Limited Liability Company (LLC): An LLC is a hybrid business structure that combines the simplicity of a sole proprietorship with the liability protection of a corporation. Unlike a sole proprietorship, the owner's personal assets are protected from the business's debts and liabilities.

- Corporation: A corporation is a separate legal entity that offers liability protection for its owners (shareholders) but is subject to double taxation (corporate income tax and personal income tax on dividends). A sole proprietorship, on the other hand, is not a separate legal entity and is subject to single taxation (personal income tax).

What are the statistics on sole proprietorship success rates?

Based on 1994-2021 data, 67.9% of new businesses survive at least two years, 49.2% survive five years, and only 25.6% survive fifteen years.

Learn More...

According to the latest SBA 2024 data covering 1994-2021, business survival rates are: 67.9% survive at least two years, 49.2% survive five years, 33.8% survive ten years, and 25.6% survive fifteen years.

Sole proprietorships, representing the majority of nonemployer firms, face even greater challenges than these general statistics suggest due to single-owner dependency.

These statistics vary significantly depending on the industry and specific circumstances of each business.

What industries are common for sole proprietorships?

Retail, professional services, home-based businesses, food service, personal care services, and creative services.

Learn More...

Popular industries for sole proprietorships include:

- Retail

- Professional services (e.g., consulting, freelance work)

- Home-based businesses (e.g., online sales, tutoring)

- Food service (e.g., catering, food trucks)

- Personal care services (e.g., hairstyling, massage therapy)

- Creative services (e.g., graphic design, photography)

How do I dissolve a sole proprietorship?

Close your business bank account, pay any remaining taxes and debts, cancel business licenses, notify stakeholders, dispose of assets, and keep records.

Learn More...

To dissolve a sole proprietorship, you must:

- Close your business bank account.

- Pay any remaining taxes, debts, and liabilities.

- Cancel business licenses and permits.

- Notify customers, suppliers, and creditors of the business closure.

- Dispose of business assets and inventory.

- Keep records of the dissolution process for tax and legal purposes.

What is the average income of a sole proprietor?

The average annual net income for a sole proprietor in the U.S. was approximately $47,000 in 2019.

Learn More...

According to data from the Internal Revenue Service (IRS), the average annual net income for a sole proprietor in the United States was approximately $47,000 in 2019.

How do sole proprietorships contribute to the economy?

Sole proprietorships provide employment, promote innovation, and contribute to local communities.

Learn More...

Sole proprietorships play an essential role in the U.S. economy by providing employment opportunities, promoting innovation, and contributing to local communities.

In 2019, sole proprietorships reported total receipts of over $1.4 trillion.

How has the number of sole proprietorships changed over time?

The number of nonemployer firms (primarily sole proprietorships) has increased dramatically by 84% since 1997.

Learn More...

According to the latest SBA 2024 data, nonemployer firms have increased by 84% since 1997, representing significant growth in sole proprietorship formation.

Currently, there are 28,477,518 nonemployer firms in the U.S., with 86.3% being sole proprietorships, meaning approximately 24.6 million sole proprietorships operate without employees.

This growth trend reflects the rise of the gig economy, remote work opportunities, and increased entrepreneurship.

What is the survival rate of minority-owned sole proprietorships compared to non-minority-owned businesses?

Minority-owned businesses have a lower survival rate than non-minority-owned businesses overall.

Learn More...

Research conducted by the Minority Business Development Agency (MBDA) indicates that minority-owned businesses have a lower survival rate than non-minority-owned businesses overall.

However, this research does not differentiate between sole proprietorships and other business structures, so it is unclear whether the same trend applies specifically to minority-owned sole proprietorships.

Are there any tax deductions specific to sole proprietorships?

There are several tax deductions that can benefit sole proprietorships, such as home office deduction, business travel expenses, vehicle expenses, and self-employed health insurance deduction.

Learn More...

While there aren't deductions exclusive to sole proprietorships, there are several tax deductions that can benefit these businesses.

- Home office deduction: If you use a portion of your home exclusively for business purposes, you may be able to deduct expenses related to that space.

- Business travel expenses: Sole proprietors can deduct costs associated with business trips, such as transportation, lodging, and meals.

- Vehicle expenses: If you use your personal vehicle for business purposes, you can either claim the standard mileage rate or actual expenses incurred (e.g., gas, maintenance).

- Self-employed health insurance deduction: If you're self-employed and pay for health insurance premiums for yourself and your dependents, you may be eligible for this deduction.

These deductions can help reduce the taxable income of a sole proprietorship, ultimately lowering the overall tax burden on the owner.

Sources

- U.S. Small Business Administration (SBA): 2022 Small Business Profile

- Bureau of Labor Statistics: Entrepreneurship and the U.S. Economy

- Internal Revenue Service (IRS): Sole Proprietorship Returns

- Lendio: 2024 Woman-Owned Business Statistics

- Statista: Number of sole proprietorship establishments in the United States from 1997 to 2020

- Minority Business Development Agency (MBDA): Failure to Launch: The Institutional Causes of Minority Entrepreneurship